The Manufacturing of Energy

A coming change in energy provision, from extraction to manufacturing, that should reduce long-term energy costs

Earlier this month Ben van Beurden, the Chief Executive of Royal Dutch Shell, made the following comments about the emerging energy business:

“He contrasts Shell’s annual $30bn investment – overwhelmingly in oil and gas – with what he says is the total $5bn annual investment of the top 10 solar companies. “These top 10 solar companies don’t make any profit, have never paid any cent of dividend in their history. So I cannot invest $15-20bn in solar and wind, which is quite often what people somehow hope us to do, and also still at same time pay a dividend. We have to find ways to make these business models work.” ‘

UK Daily Telegraph, 2 July 2016

The Shell boss is probably right to say that its unlikely that incumbent oil companies will be able to transform effectively into profitable solar and wind firms. As argued here history shows that developing into your own competition is a rare phenomenon. Dong Energy and Total are making moves in this direction, but its unlikely many large oil companies will change their main functioning model any time soon.

However, the nature of energy competition is changing, and whilst Mr van Beurden may not approve of the size or profitability of his competitors in adjacent energy markets, he may be wise to take a closer look at them.

That’s mainly because the structure of competition is exactly the opposite of the current oil industry model of extraction – it’s based on manufacturing. Or put another way, it’s the distinction between negative experience curves, and positive ones.

Synchronised Extraction

The dominant energy model oil and gas has two core elements: extraction and simultaneous development.

Oil and gas firms rely on the large-size extraction of fossil fuels, normally using complex, high cost projects to deliver the scale that allows big production hikes and hence revenue growth. In the past, both national oil companies (NOCs) and international oil company majors (IOCs) have made these work at reasonable costs – making profits at historically average oil prices of about $35-50/bbl.

Large national oil companies are still able to work at these historic prices, especially OPEC, as they have full rights to very large reservoirs of most of the world’s oil. Most of these oil-fields are onshore in and relatively simple to exploit.

IOCs, on the other hand, cannot manage at current prices, having cancelled over $500bn of large projects in the past 2 years, and, along with their suppliers, laying off over 300,000 workers.

Having access now only to difficult, remote and extreme reservoirs – offshore deepwater, Arctic, high pressure and so on – they have to resort to bigger, and more complex extraction projects. However, as noted here these types of large, single-size, static projects require formidable abilities to manage in both construction and operation.

As a result, the IOC big extraction business model of the past decade has demonstrated a negative experience curve – in line with similar large projects in other industries: that is, the cost of production is going up over time, rather than reducing. In 2005 Shell invested $15bn of capex for 3.5mboepd of production – by 2015 capex had increased to over $29bn, but production had fallen to 2.95mboepd – a cost factor per barrel increase of over 230%, or 10% increase per annum in real terms. Most other IOCs have similar statistics.

None of the IOC megaprojects exhibit any of the critical features of experience curve improvements: standardization, identical design, near-identical construction experience. Quite the opposite: designs and processing units are often customized and unique and constructed in a huge variety of circumstances – greenfield sites, brownfield locations, dedicated yards, offshore and so on.

These projects are engineering marvels in their own way, but they come at a heavy cost: large LNG plants for example have increased from $500-600mt pa in 2004 to typically over $2,000-3,000/mt pa today.

As a result whilst the large majors have sunk over $3 trillion dollars in capex, they have not increased production – it has remained flat. This has led to reserves to production ratios to decline, and reserves additions to drop below 100%. As the EIA chart below shows, the IOCs have struggled to replace reserves for several years now, and reserves to production ratios are now as low as 10 years and declining.

Synchronised Strategies

The extraction model has also been one of concentrated management and investment. Given the high risks of oil field development and high capital costs required, most production comes from a few large state oil companies, and a few large international firms who mainly self-finance from production revenues.

In terms of oil, this means that about 65% of global production is managed by only about 20 large firms. Historically, this has led to concerns about cartel behavior from OPEC artificially keeping oil prices high from restrained production. These concerns have diminished in the past few years, but the model is still susceptible to coordinated thinking and low diversity of approach to technology and strategy.

Most of the oil companies use only a handful of large suppliers for engineering, procurement, wells delivery and construction activities. They also pursue similar management strategies, and tend to invest and disinvest in concert, reading the market and impact on their financial model in roughly the same way – hence downturns and upturns tends to have synchronized reactions which exacerbate issues such as postponed investment and job losses.

There are some outliers, but the large extraction model coupled with a uniform business approach to use megaprojects for production growth has been the dominant energy model this century.

The concern from Mr van Beurden is therefore not about competition per se – all oil companies even in a concentrated business context have had to deal with competitors. It’s the fact that the competition does not look anything like the incumbent model, making it difficult to respond to.

A New Model – Dispersed Manufacturing

Compared to the predominant model of large-scale coordinated extraction, the newest form of energy is the exact opposite – small, scalable, dispersed and based on manufacturing rather than extraction.

This model of manufactured energy also straddles the fossil fuel and the non-fossil fuel sectors: the main examples being shale oil and gas wells, but also also wind farms and solar PV arrays.

These approaches to energy creation display key features that allow their costs to reduce rapidly over time: template standardization, a large series of similar designs, and a large number of near-identical experiences in their manufacture that lead to rapid technological learning.

Each of these technologies has been a long time coming, and it has been possible to write them off as always being on the edge of adoption, but never getting there.

What has changed in the past decade is that both sources – shale oil and gas and wind plus PV solar – have attained tipping point unit cost reductions through relentless experience curve cost decreases. And this has allowed them to now at last quickly grow into the energy markets and scale up.

The experience curve benefits look similar across different energy markets.

Transport

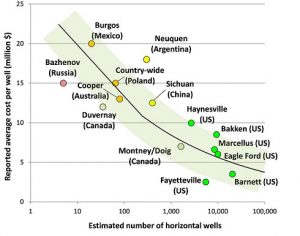

For shale producers, a major break-through was reaching break-even costs of around $80-90/bbl in 2010. As noted in Russell Gold’s book, The Boom, this was supported by deep financial markets, and governmental policy around land access as well, hence the US expertise may not transfer easily. But in the US, this combination, shielded by high oil prices (and gas prices linked to them), allowed the key process of empirical trial and error to take place, and the rapid learnings to push down unit drilling costs for oil and gas via fracking – see chart.

In addition, these factors allowed small players to enter the energy production business at a relatively small scale. Although many succumbed to bankruptcies, and many still do, the cumulative experience of this dispersed manufacturing model allowed an overall system of cost reduction and knowledge transfer to occur.

In fact, this is often true of any emergent technology, such as the wide range of on-line start-ups that failed, but left the legacy of the modern internet .

The tens of failed shale oil firms that “never made any profit, or paid a cent of dividend in their history” are creating the future blueprint and technological legacy for next generation companies to leverage. It’s what Ruchir Sharma labeled a “good binge” in his work “Rise and Fall of Nations”

Results have been exceptional. As a collective, the shale industry spent only a tenth of the capital of the oil majors in 2010-2015, yet produced a net increase of over 5 million boepd. This is the equivalent of a new Iraq in 5 years, and along with a reduction in demand from China, caused oil prices to halve, and the global oil and gas markets to become far more competitive. In the past two years this has moved over $3 trillion from the pockets of producers to consumers globally, and allowed the US to become an energy exporter for the first time in decades.

In addition, the dispersed and scalable nature of the model created diverse and more rapid decision-making and strategies (1). Many firms pursued similar design and fracking techniques aiding unit cost declines, but they also used different strategies and approaches eg types of financing, or timing choices of areas for development.

This meant that when oil prices fell, they did not just respond in similar ways – and being able to scale up as well as scale-down, they could regulate and temper their reactions, avoiding a single coordinated answer to the downturn that intensifies the issues.

As a result, they continued to increase production in 2014 and 2015 by over 2.5mboepd, whilst major firms cancelled projects, and saw production level off. Today bankruptcies continue, and production has declined, but its clear also that several of the shale oil and gas firms are finding new ways back to production at varying scales using even cheaper techniques, far more quickly than the large-scale extraction alternatives.

Incumbent energy firms mis-read this new style of competition because it refused to match the form they expected it to take – it did not appear as a new large extraction technology or entity, it emerged gradually and collectively and at a small scale that could develop and in aggregate produce a major new source of energy.

LNG

Shale gas production via the manufacturing route in the US has also been highly disruptive. LNG is the world’s second largest traded commodity after crude oil, but largely based on long-term contracts and linked to oil prices. The long-term relationships are required, historically, due to the heavy investment and extended project time-frame required to create LNG plants.

US shale gas changes all that. Therapid growth of the shale resource has propelled the US to now being an LNG exporter, as domestic supplies are saturated. In addition, the multiple, dispersed manufacturing model means shipment go US LNG can respond more flexibly to market demand, removing the need for buyers to enter into long-term agreements.

As a result, the US is expected to be the third largest exporter of LNG with 14% of global trade by 2020 – from having virtually no presence in the market in 2015.

This puts more pressure on global LNG prices, and shifts the market emphasis toward spot trading, and away from price linkages to crude oil.

The disruptive manufacturing model allows aggregated demand, and flexible supply through scalability – the opposite of the incumbent model.

Power

The global power sector is another case of the rise of dispersed manufacturing, along with financing and government policy.

High fossil fuel prices of the past decade have also allowed alternative energy firms to experiment with technology, but policies aimed at low or zero-carbon targets have also been a major factor.

The experience curve has worked on top of this and driven down costs that make the manufacturing of wind and solar power a viable alternative for companies and countries to consider.

The technology follows the same pattern of shale oil and gas: standardised design templates, a large series of similar design and near-identical manufacturing and installation methods.

It differs in one key respect however from shale: the energy being manufactured leads to fuel-less electricity, not a finite form of fuel.

The impact of hitting a manufacturing tipping point in terms of cost have led to wind and solar technologies providing the bulk of the growth in power sector markets. Since 2000 for example PV solar costs have reduced by 80% to around $100/MWh, or a 20% reduction every 2-3 years, making them viable with gas and coal equivalents. As a result investment in power via renewable energy has been double the fossil fuel investment overt the past 8 years (see below).

source Bloomberg, T Randall.

But the actual unit cost benefits need to be also assessed in terms of business model. Most solar and wind companies have struggled to make consistent profits as Shell point out. Over a hundred have gone bankrupt in the past decade.

Like shale, however, having reached a tipping point of cost parity with extraction technologies, the experience curve does not stop. The learning curve of manufacturing technology suggests that this cost reduction will continue over the next two decades, eg for Solar PV below.

The pace of investment is still therefore estimated to average $250bn per year over the next 25 years in comparison to $100bn from fossil fuels (mainly coal and gas). By 2040, using this prediction, about 60% of power capacity globally will derive from these types of scalable, dispersed manufactured energy sources, and aggregate investment is estimated at $7.4 trillion, versus $ 3.2 trillion for fossil fuels and nuclear – with growth greatest in Asia Pacific and non-OECD regions.

The business model will also continue to rely on dispersed and scalable (large and small) technology development, diverse business strategies and policy support. This means, like shale it is increasingly unreliant on a high fossil fuel price. For a start, wind and solar do not compete with oil directly (yet), and secondly, their experience curve will continue to drive down costs, irrespective of the price movements of competitors. The choice of whether to use them or not will be driven by other factors such as policy and local endowment.

Shale oil and gas and wind and solar technologies have shown that in both oil and gas sectors the power of dispersed, scalable, manufacturing techniques are now of a mature enough magnitude to compete directly with the historical large, single-sized, extraction model.

It is not only about a different technology itself, but the financial investment options, diverse company strategies, multiple scales of entry and experience curve momentum that these new technologies also allow.

A snapshot of power projects underway in 2016 in the US summarises the state of play.

source EIA

Of about 26GW of new power capacity to be added this year (about 2.5% of the current capacity), 16GW or 60% will be from wind and solar, and a third from natural gas. The map below shows the size and distribution of the projects. Its clear the wind and solar projects are far more numerous and smaller, than the more concentrated gas projects (plus one nuclear).

As discussed, the distributed, scalable manufacturing model is a different form of energy power creation – the manufacture of energy conversation equipment, rather than the extraction of fuel and supply to large plant. Its scale is in aggregate, rather than single site, and it continues to follow experience cost curves and multiple business models.

The Manufacturing of Energy

The transition of energy from purely extraction to manufacturing methods drives greater cost control.

It’s a world of opposites: technologically from big, one-sized, long-term, unique and concentrated projects to scalable, rapid, replicable and dispersed ones.

Managerially it moves from centralized, coordinated planning to diverse, uncoordinated decision-making.

And financially the focus develops from major capex expenditures and dividend growth to an array of investment models of differing magnitudes.

The impact should be significant

A stylized summary of the entry of manufacturing models – shale, solar, wind – into the transport and power sectors is shown below on a percentage ratio basis only. The data assumes the BNEF 60% power market from renewables by 2040, and EV growth to 35% of global vehicle sales by 2040 – with 60% of the electric in EVs from renewables. It also assumes US shale oil and gas retain their current production levels.

Whatever the actual proportions, its clear that there is significant potential for the scalable manufacturing model to impact the cost and distribution of energy development.

source www.dollarsperbbl.com analysis

A further process of creative destruction seems to be underway. The analog model of extraction and large investment is at least sharing a platform with a more digital, scalable form of energy production. Over time, this should reduce price volatility in energy markets heavily exposed to extractive fuel prices such as transport and LNG. The increase in competitive technologies in the power sector also indicates that energy production costs should decrease there also.

However, whether this results in price decreases, at least in the short-term, is dependent on other factors – legacy infrastructure, local endowment of energy eg coal or oil, and governmental and inter-governmental policies.

But the rise of manufacturing technology in the energy sector is in principle a positive development, whether in shale or wind or solar.

It moves the cost of production further into the experience curve of technology and engineering and away from the increasing costs of extraction – this indicates long-term energy cost productivity improvements and so lower costs.The scalability of the manufacturing model will also create more flexible pricing, potentially attenuating price volatility.

Conclusion – If the long range average price of extractive (oil and gas) energy was around $40-50/bbl, the future mix of manufactured and extracted energy should be lower, more flexible, scalable and more productive.

What this means for the incumbent extraction model is the subject of an upcoming post.

——————–

Notes:

(1) – this point inspired from a conversation with Liam Denning, Bloomberg Gadly (Energy)